Free Michigan Mi 2210 Template in PDF

The Michigan MI-2210 form is an essential document for taxpayers who may have underpaid their estimated income tax throughout the year. It is specifically designed to help individuals and fiduciaries calculate any penalties and interest that may arise from underpayment. Issued by the Michigan Department of Treasury under the authority of the Income Tax Act of 1967, this form must be attached to the MI-1040 or MI-1041 tax returns. Taxpayers should be aware that if their underpayment is $500 or less, they are not required to complete this form. The MI-2210 guides users through a series of calculations, starting with determining the estimated tax required for the year and comparing it against actual payments made. It breaks down the process into manageable parts, allowing for a clear assessment of any remaining underpayments and the corresponding interest owed. Additionally, taxpayers can choose to annualize their income if it varies significantly throughout the year, which can affect their estimated tax obligations. Understanding this form is crucial for avoiding unnecessary penalties and ensuring compliance with Michigan tax laws.

Form Example

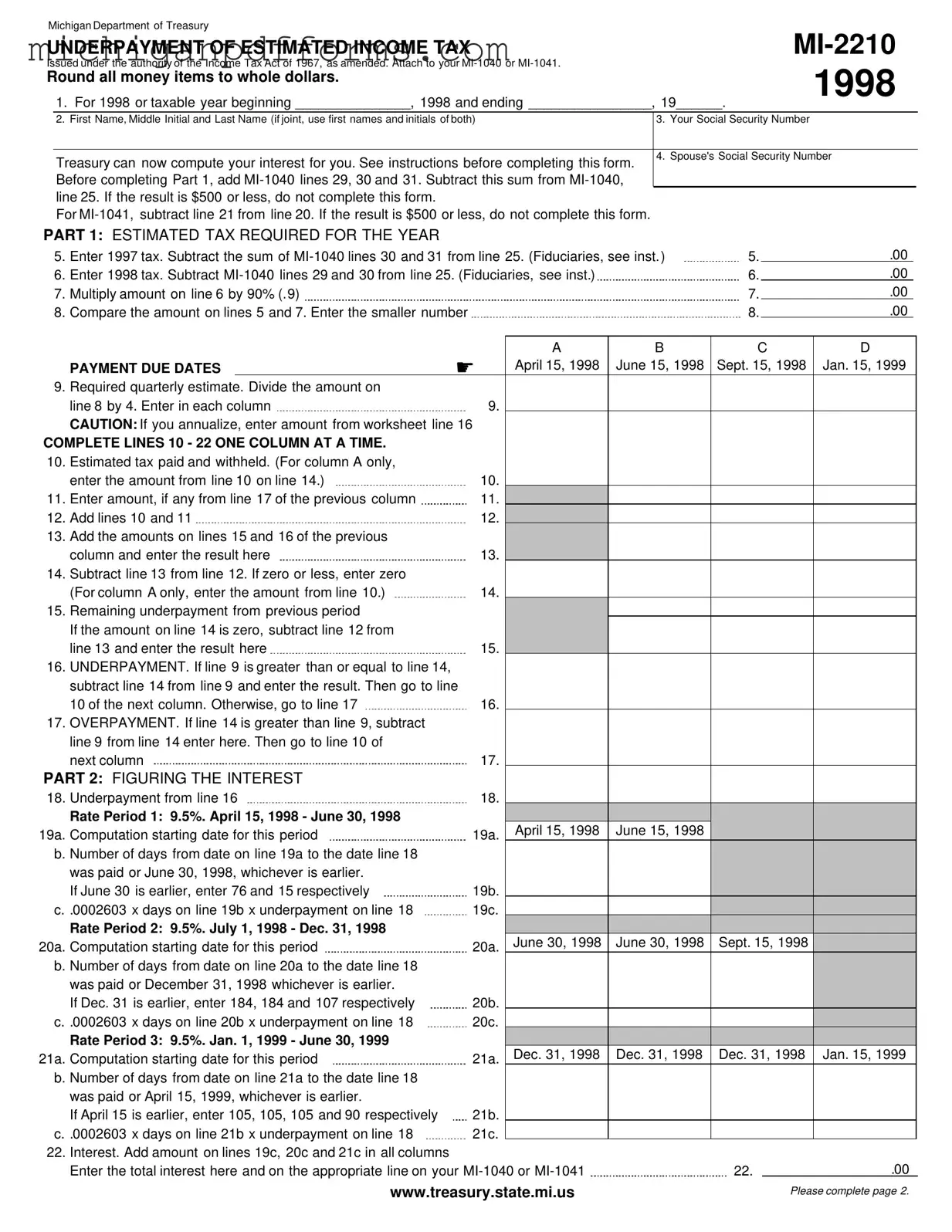

Michigan Department of Treasury

UNDERPAYMENT OF ESTIMATED INCOME TAX

Issued under the authority of the Income Tax Act of 1967, as amended. Attach to your

Round all money items to whole dollars.

1. For 1998 or taxable year beginning _______________, 1998 and ending ________________, 19______.

1998

|

2. |

First Name, Middle Initial and Last Name (if joint, use first names and initials of both) |

|

|

3. Your Social Security Number |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Treasury can now compute your interest for you. See instructions before completing this form. |

4. Spouse's Social Security Number |

|||||||||

|

|

|

|

|

|||||||

|

Before completing Part 1, add |

|

|

|

|

||||||

|

line 25. If the result is $500 or less, do not complete this form. |

|

|

|

|

|

|

|

|

||

|

For |

|

|

|

|

||||||

PART 1: ESTIMATED TAX REQUIRED FOR THE YEAR |

|

|

|

|

|

|

|

|

|||

5. |

Enter 1997 tax. Subtract the sum of |

5. |

|

.00 |

|||||||

6. |

Enter 1998 tax. Subtract |

|

|

6. |

|

.00 |

|||||

7. |

Multiply amount on line 6 by 90% (.9) |

|

|

|

|

|

7. |

|

.00 |

||

8. |

Compare the amount on lines 5 and 7. Enter the smaller number |

|

|

|

|

8. |

|

.00 |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A |

|

B |

C |

D |

|

|

|

PAYMENT DUE DATES |

|

☛ |

April 15, 1998 |

June 15, 1998 |

Sept. 15, 1998 |

Jan. 15, 1999 |

|||

9. |

Required quarterly estimate. Divide the amount on |

|

|

|

|

|

|

|

|

||

|

|

line 8 by 4. Enter in each column |

|

9. |

|

|

|

|

|

|

|

|

|

CAUTION: If you annualize, enter amount from worksheet line 16 |

|

|

|

|

|

|

|

||

COMPLETE LINES 10 - 22 ONE COLUMN AT A TIME. |

|

|

|

|

|

|

|

|

|||

10. |

Estimated tax paid and withheld. (For column A only, |

|

|

|

|

|

|

|

|

||

|

|

enter the amount from line 10 on line 14.) |

|

10. |

|

|

|

|

|

|

|

11. |

Enter amount, if any from line 17 of the previous column |

|

11. |

|

|

|

|

|

|

||

12. |

Add lines 10 and 11 |

|

12. |

|

|

|

|

|

|

||

13. |

Add the amounts on lines 15 and 16 of the previous |

|

|

|

|

|

|

|

|

||

|

|

column and enter the result here |

|

13. |

|

|

|

|

|

|

|

14. |

Subtract line 13 from line 12. If zero or less, enter zero |

|

|

|

|

|

|

|

|

||

|

|

(For column A only, enter the amount from line 10.) |

|

14. |

|

|

|

|

|

|

|

15. |

Remaining underpayment from previous period |

|

|

|

|

|

|

|

|

||

|

|

If the amount on line 14 is zero, subtract line 12 from |

|

|

|

|

|

|

|

|

|

|

|

line 13 and enter the result here |

|

15. |

|

|

|

|

|

|

|

16. |

UNDERPAYMENT. If line 9 is greater than or equal to line 14, |

|

|

|

|

|

|

|

|

||

|

|

subtract line 14 from line 9 and enter the result. Then go to line |

|

|

|

|

|

|

|

||

17. |

10 of the next column. Otherwise, go to line 17 |

|

16. |

|

|

|

|

|

|

||

OVERPAYMENT. If line 14 is greater than line 9, subtract |

|

|

|

|

|

|

|

|

|||

|

|

line 9 from line 14 enter here. Then go to line 10 of |

|

|

|

|

|

|

|

|

|

|

|

next column |

|

17. |

|

|

|

|

|

|

|

PART 2: FIGURING THE INTEREST |

|

|

|

|

|

|

|

|

|||

18. |

Underpayment from line 16 |

|

18. |

|

|

|

|

|

|

||

|

|

Rate Period 1: 9.5%. April 15, 1998 - June 30, 1998 |

|

|

|

|

|

|

|

|

|

19a. |

Computation starting date for this period |

|

19a. |

April 15, 1998 |

June 15, 1998 |

|

|

|

|||

|

b. Number of days from date on line 19a to the date line 18 |

|

|

|

|

|

|

|

|

||

|

|

was paid or June 30, 1998, whichever is earlier. |

|

|

|

|

|

|

|

|

|

|

|

If June 30 is earlier, enter 76 and 15 respectively |

|

19b. |

|

|

|

|

|

|

|

|

c. .0002603 x days on line 19b x underpayment on line 18 |

|

19c. |

|

|

|

|

|

|

||

|

|

Rate Period 2: 9.5%. July 1, 1998 - Dec. 31, 1998 |

|

|

|

|

|

|

|

|

|

20a. |

Computation starting date for this period |

|

20a. |

June 30, 1998 |

June 30, 1998 |

Sept. 15, 1998 |

|

||||

|

b. Number of days from date on line 20a to the date line 18 |

|

|

|

|

|

|

|

|

||

|

|

was paid or December 31, 1998 whichever is earlier. |

|

|

|

|

|

|

|

|

|

|

|

If Dec. 31 is earlier, enter 184, 184 and 107 respectively |

|

20b. |

|

|

|

|

|

|

|

|

c. .0002603 x days on line 20b x underpayment on line 18 |

|

20c. |

|

|

|

|

|

|

||

|

|

Rate Period 3: 9.5%. Jan. 1, 1999 - June 30, 1999 |

|

|

|

|

|

|

|

|

|

21a. |

Computation starting date for this period |

|

21a. |

Dec. 31, 1998 |

Dec. 31, 1998 |

Dec. 31, 1998 |

Jan. 15, 1999 |

||||

|

b. Number of days from date on line 21a to the date line 18 |

|

|

|

|

|

|

|

|

||

|

|

was paid or April 15, 1999, whichever is earlier. |

|

|

|

|

|

|

|

|

|

|

|

If April 15 is earlier, enter 105, 105, 105 and 90 respectively |

|

21b. |

|

|

|

|

|

|

|

|

c. .0002603 x days on line 21b x underpayment on line 18 |

|

21c. |

|

|

|

|

|

|

||

22. |

Interest. Add amount on lines 19c, 20c and 21c in all columns |

|

|

|

|

|

|

|

|

||

|

|

Enter the total interest here and on the appropriate line on your |

|

|

22. |

|

.00 |

||||

www.treasury.state.mi.us |

Please complete page 2. |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

A |

B |

C |

D |

|

PART 3: FIGURING THE PENALTY |

|

April 15, 1998 |

June 15, 1998 |

Sept. 15, 1998 |

Jan. 15, 1999 |

||

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

23. |

Underpayment (see instructions) |

23. |

.00 |

.00 |

.00 |

.00 |

|

% |

% |

% |

% |

||||

24. |

Enter 25% (.25) or 10% (.10) (see instructions) |

24. |

|||||

.00 |

.00 |

.00 |

.00 |

||||

25. |

Multiply amount on line 23 by line 24 |

25. |

|||||

26. |

TOTAL PENALTY. Add line 25, column A - D. Enter total penalty in appropriate space |

|

|

|

on the pay line of your |

26. |

.00 |

27. |

Add lines 22 and 26. This is your total penalty and interest to be added to your tax due |

27. |

.00 |

This form computes penalty and interest for estimate vouchers to the date of payment or April 15, 1999, whichever is earlier. Additional penalty and interest for late filing accrues on your annual return from April 15 to the date of payment.

ANNUALIZED INCOME

Taxpayers who receive income unevenly during the year (for example, from a seasonal business, capital gain, severance pay or bonus) may benefit by completing this worksheet. If you use this method, you must annualize for the entire year by completing all four columns.

If you choose to annualize your income, you must attach this worksheet and a completed

As you complete the worksheet remember the following.

Line 1 must be the

Example: You earned $5,000 in the first three months of the year. You earned an additional $4,000 during April and May. Enter on worksheet line 1, $5,000 in the first column and $9,000 in the second column.

Each entry on worksheet line 12 will be

Taxpayers who annualize must also enter 25 percent of tax withheld in each column of the

ANNUALIZED INCOME WORKSHEET (Complete one column at a time.)

Line numbers refer to this worksheet unless another form is |

|

|

|

|

|

|

listed. Estates and trusts do not use the period ending date |

|

|

|

|

|

|

|

|

|

|

|

|

|

shown to the right. Instead, use the following: 2/28/98, 4/30/98, |

|

First 3 mos. |

First 5 mos. |

First 8 mos. |

All 12 mos. |

|

7/31/98 and 12/1/98. |

|

|||||

1. Enter the total income subject to tax (reported on your 1998 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

corresponding column |

1. |

|

|

|

|

|

2. Annualization amounts |

2. |

4 |

2.4 |

1.5 |

1 |

|

3. Annualized income. Mutliply line 1 by line 2 |

3. |

|

|

|

|

|

4. Enter your total exemption allowance |

4. |

|

|

|

|

|

5. Subtract line 4 from line 3 |

5. |

|

|

|

|

|

6. Multiply line 5 by 1998 tax rate of 4.4% (.044) |

6. |

|

|

|

|

|

7. Enter the sum of your 1998 |

7. |

|

|

|

|

|

8. Subtract line 7 from line 6 (if zero or less, enter "0") |

8. |

|

|

|

|

|

9. Multiply amount from line 8 by 22.5% (1st period), |

|

(line 8 x 22.5%) |

(line 8 x 45%) |

(line 8 x 67.5%) |

(line 8 x 90%) |

|

45% (2nd period), 67.5% (3rd period) and 90% (4th period). |

|

|

|

|

|

|

Enter the results in each column |

9. |

|

|

|

|

|

10. Enter combined amounts from line 16 of all previous columns |

10. |

|

|

|

|

|

11. Subtract line 10 from line 9. If less than zero, enter zero "0" |

11. |

|

|

|

|

|

12. Divide the amount on |

|

|

|

|

|

|

result in each column |

12. |

|

|

|

|

|

13. Enter the amount from line 15 of the previous column |

13. |

|

|

|

|

|

14. Add lines 12 and 13 |

14. |

|

|

|

|

|

15. Subtract line 11 from line 14. If less than zero, enter zero "0" |

15. |

|

|

|

|

|

16. Enter the smaller of lines 14 or 11 here and on |

16. |

|

|

|

|

|

GENERAL INSTRUCTIONS

Use this form to see if you owe penalty and interest for failing to make estimated payments or for underpaying the estimated tax due. You can be charged interest (and possibly penalty) if your payment was low or late in any quarter. This is true even if you are due a refund when you file your tax return. The interest and penalty are figured separately for each due date. So you could still owe interest and penalty even if you made up an earlier underpayment with an overpayment later.

Because this is a complicated form, you may choose to have Treasury compute your interest and penalty and send you a bill instead of filing the form yourself. If you want Treasury to figure your interest, complete your

If you annualize your income, you must complete the

You may avoid penalty and interest and should not file this form if:

1.You had no tax liability for 1997 (if you had to file), or you were not required to file a 1997 return and your 1997 federal tax return was for a full 12 months.

2.The total tax on your 1998 return minus the amount you paid in withholding and all your credits is $500 or less.

3.The amounts of tax withheld and timely estimated tax payments made in equal installments equal at least 90 percent of the tax due in 1998 or 100 percent of the tax due in 1997, unless the installment due in any period is paid later than the due date of that installment.

Special rules for farmers, fishermen and seafarers.

Do not file this form if BOTH of these apply:

1.Your gross income from farming, fishing or seafaring is at least 2/3 of your annual gross income for 1997 or 1998, AND

2.You filed your

If you need to file estimated tax, request a 1999 Michigan estimated income tax formset

Before completing Part 1, add

Part 1. FIGURING THE UNDERPAYMENT

Line 5: Figure your 1997 tax from your 1997 return. On the

Line 6: Figure your 1998 tax. On the

Line 9: If you did not receive your income evenly throughout the year, you may annualize your income. See the instructions and worksheet on this form. The sum of the four installments must equal the lowest of:

•90 percent of the tax shown on your 1998 tax return, OR

•100 percent of the tax shown on your 1997 tax return.

Line 10: Enter the estimated tax payments you made plus any withholding. Note:

•

•An overpayment from 1997 that has been credited forward to 1998 will be applied to the first installment.

•Do not enter extension payments on this form.

(CONTINUED ON BACK.)

In column A, enter the estimated tax payments made by April 15, 1998 that were for the 1998 tax year. In column B, enter payments made after April 15 and through June 15, 1998. In column C, enter payments made after June 15 and through September 15, 1998. In column D, enter payments made after September 15 and through January 15, 1999. Extension payments or other payments received after January 15 are not considered estimate payments.

Part 2. FIGURING THE INTEREST

The

Lines

Example: Your tax due each period is $2,000. You have an underpayment of $1,000 for the first period (due April 15). On June 10 you send $2,000 to pay the second installment. But, $1,000 of this payment goes toward your $1,000 underpayment first. Interest is computed on $1,000 from April 15 to June 10 (56 days). The remaining $1,000 is applied to your second installment payment, creating a second period underpayment of $1,000. Interest will continue to accrue on this $1,000 until another payment is received.

Interest rates are set by Treasury twice each year for

For example, if the Michigan prime rate is 10.2 percent, your interest rate for completing the

interest rates, request REVENUE ADMINISTRATIVE BULLETIN

Part 3. FIGURING THE PENALTY

Penalty is 25 percent of the tax due for failing to file estimated payments, or 10 percent for failing to pay enough with your estimates or paying late.

Line 23: The underpayment for the penalty charge is figured in the same general way as the under- payment for interest.

Exceptions:

•Payments are applied in the quarter they are received.

•If an overpayment occurs in any quarter, the overpayment amount is carried forward to the next quarter and applied as a timely payment.

•Payments are not carried back to offset underpayments in previous quarters.

The amount on line 23 cannot be less than zero (0).

Line 24: Enter 25 percent if estimated tax payments were not made for 1998. Enter 10 percent if estimated tax payments were made for 1998.

Example: In the example in Part 2, the $2,000 payment received on June 10 is applied to the $2,000 required payment in the second quarter. The penalty in the first quarter is $100 (10 percent of the $1,000 underpayment in the first quarter). The penalty in the second quarter would be zero (0).

Document Specs

| Fact Name | Details |

|---|---|

| Purpose | The MI-2210 form is used to calculate penalties and interest for underpayment of estimated income tax in Michigan. |

| Governing Law | This form is issued under the authority of the Income Tax Act of 1967, as amended. |

| Filing Requirement | Attach the MI-2210 to your MI-1040 or MI-1041 when filing your tax return. |

| Threshold for Completion | If the underpayment result is $500 or less, do not complete this form. |

| Interest Rates | The interest rate for underpayment is set by Treasury and is typically 1% above the prime rate in Michigan. |

| Quarterly Due Dates | Estimated tax payments are due on April 15, June 15, September 15, and January 15 of the following year. |

| Annualization Option | Taxpayers with uneven income may choose to annualize their income, requiring additional documentation. |

Fill out Common Templates

Michigan Unemployment for Employers - Direct lines of communication with the Inquiry Line demonstrate the UIA’s commitment to providing guidance and assistance as needed.

Michigan Des 025 - It serves individuals involved in driver education or third-party testing roles, requiring fingerprints for state certification.

To ensure a smooth eviction process, it is vital for landlords to utilize the correct paperwork, such as the Illinois PDF Forms, which guide you in creating a valid Notice to Quit that complies with state regulations and provides tenants with clear instructions on vacating the premises.

Michigan Pedigree - Designed to capture detailed ancestral information including places of birth, marriage, and death.